PortfolioCVaR

Creates PortfolioCVaR object for conditional value-at-risk portfolio optimization and analysis

Description

Use PortfolioCVaR to create a

PortfolioCVaR object for conditional value-at-risk portfolio

optimization.

The main workflow for CVaR portfolio optimization is to create an instance of a

PortfolioCVaR object that completely specifies a portfolio

optimization problem and to operate on the PortfolioCVaR object using

supported functions to obtain and analyze efficient portfolios. For details on this

workflow, see PortfolioCVaR Object Workflow.

You can use the PortfolioCVaR object in several ways. To set up a

portfolio optimization problem in a PortfolioCVaR object, the

simplest syntax

is:

p = PortfolioCVaR;

PortfolioCVaR object, p, such

that all object properties are empty. The PortfolioCVaR object also accepts collections of name-value

pair arguments for properties and their values. The PortfolioCVaR

function accepts inputs for properties with the general

syntax:

p = PortfolioCVaR('property1',value1,'property2',value2, ... );If a PortfolioCVaR object already exists, the syntax permits the

first (and only the first argument) of the PortfolioCVaR object to be

an existing object with subsequent name-value pair arguments for properties to be added

or modified. For example, given an existing PortfolioCVaR object in

p, the general syntax

is:

p = PortfolioCVaR(p,'property1',value1,'property2',value2, ... );

Input argument names are not case sensitive, but must be completely specified. In

addition, several properties can be specified with alternative argument names (see Shortcuts for Property Names). The

PortfolioCVaR object tries to detect problem dimensions from the

inputs and, once set, subsequent inputs can undergo various scalar or matrix expansion

operations that simplify the overall process to formulate a problem. In addition, a

PortfolioCVaR object is a value object so that, given portfolio

p, the following code creates two objects, p

and q, that are

distinct:

q = PortfolioCVaR(p, ...)

After creating a PortfolioCVaR object, you can use the associated

object functions to set portfolio constraints, analyze the efficient frontier, and

validate the portfolio model.

For more detailed information on the theoretical basis for conditional value-at-risk portfolio optimization, see Portfolio Optimization Theory.

Creation

Description

p = PortfolioCVaRPortfolioCVaR object for conditional value-at-risk

portfolio optimization and analysis. You can then add elements to the

PortfolioCVaR object using the supported "add" and

"set" functions. For more information, see Creating the PortfolioCVaR Object.

p = PortfolioCVaR(Name,Value)PortfolioCVaR object (p) and

sets Properties using name-value

pairs. For example, p =

PortfolioCVaR('AssetList',Assets(1:12)). You can specify

multiple name-value pairs.

p = PortfolioCVaR(p,Name,Value)PortfolioCVaR object (p)

using a previously created PortfolioCVaR object

p and sets Properties using name-value

pairs. You can specify multiple name-value pairs.

Input Arguments

Output Arguments

Properties

Object Functions

setAssetList | Set up list of identifiers for assets |

setInitPort | Set up initial or current portfolio |

setDefaultConstraints | Set up portfolio constraints with nonnegative weights that sum to 1 |

estimateAssetMoments | Estimate mean and covariance of asset returns from data |

setCosts | Set up proportional transaction costs for portfolio |

addEquality | Add linear equality constraints for portfolio weights to existing constraints |

addGroupRatio | Add group ratio constraints for portfolio weights to existing group ratio constraints |

addGroups | Add group constraints for portfolio weights to existing group constraints |

addInequality | Add linear inequality constraints for portfolio weights to existing constraints |

getBounds | Obtain bounds for portfolio weights from portfolio object |

getBudget | Obtain budget constraint bounds from portfolio object |

getCosts | Obtain buy and sell transaction costs from portfolio object |

getEquality | Obtain equality constraint arrays from portfolio object |

getGroupRatio | Obtain group ratio constraint arrays from portfolio object |

getGroups | Obtain group constraint arrays from portfolio object |

getInequality | Obtain inequality constraint arrays from portfolio object |

getOneWayTurnover | Obtain one-way turnover constraints from portfolio object |

setGroups | Set up group constraints for portfolio weights |

setInequality | Set up linear inequality constraints for portfolio weights |

setBounds | Set up bounds for portfolio weights for portfolio |

setMinMaxNumAssets | Set cardinality constraints on the number of assets invested in a portfolio |

setBudget | Set up budget constraints for portfolio |

setConditionalBudget | Set up conditional budget constraints for portfolio |

setCosts | Set up proportional transaction costs for portfolio |

setDefaultConstraints | Set up portfolio constraints with nonnegative weights that sum to 1 |

setEquality | Set up linear equality constraints for portfolio weights |

setGroupRatio | Set up group ratio constraints for portfolio weights |

setInitPort | Set up initial or current portfolio |

setOneWayTurnover | Set up one-way portfolio turnover constraints |

setTurnover | Set up maximum portfolio turnover constraint |

checkFeasibility | Check feasibility of input portfolios against portfolio object |

estimateBounds | Estimate global lower and upper bounds for set of portfolios |

estimateFrontier | Estimate specified number of optimal portfolios on the efficient frontier |

estimateFrontierByReturn | Estimate optimal portfolios with targeted portfolio returns |

estimateFrontierByRisk | Estimate optimal portfolios with targeted portfolio risks |

estimateFrontierLimits | Estimate optimal portfolios at endpoints of efficient frontier |

plotFrontier | Plot efficient frontier |

estimatePortReturn | Estimate mean of portfolio returns |

estimatePortRisk | Estimate portfolio risk according to risk proxy associated with corresponding object |

setSolver | Choose main solver and specify associated solver options for portfolio optimization |

setProbabilityLevel | Set probability level for VaR and CVaR calculations |

setScenarios | Set asset returns scenarios by direct matrix |

getScenarios | Obtain scenarios from portfolio object |

simulateNormalScenariosByData | Simulate multivariate normal asset return scenarios from data |

simulateNormalScenariosByMoments | Simulate multivariate normal asset return scenarios from mean and covariance of asset returns |

estimateScenarioMoments | Estimate mean and covariance of asset return scenarios |

estimatePortVaR | Estimate value-at-risk for PortfolioCVaR object |

estimatePortStd | Estimate standard deviation of portfolio returns |

Examples

You can create a PortfolioCVaR object, p, with no input arguments and display it using disp.

p = PortfolioCVaR; disp(p);

PortfolioCVaR with properties:

BuyCost: []

SellCost: []

RiskFreeRate: []

ProbabilityLevel: []

Turnover: []

BuyTurnover: []

SellTurnover: []

NumScenarios: []

Name: []

NumAssets: []

AssetList: []

InitPort: []

AInequality: []

bInequality: []

AEquality: []

bEquality: []

LowerBound: []

UpperBound: []

LowerBudget: []

UpperBudget: []

GroupMatrix: []

LowerGroup: []

UpperGroup: []

GroupA: []

GroupB: []

LowerRatio: []

UpperRatio: []

MinNumAssets: []

MaxNumAssets: []

ConditionalBudgetThreshold: []

ConditionalUpperBudget: []

BoundType: []

This approach provides a way to set up a portfolio optimization problem with the PortfolioCVaR function. You can then use the associated set functions to set and modify collections of properties in the PortfolioCVaR object.

You can use the PortfolioCVaR object directly to set up a “standard” portfolio optimization problem. Given scenarios of asset returns in the variable AssetScenarios, this problem is completely specified as follows:

m = [ 0.05; 0.1; 0.12; 0.18 ];

C = [ 0.0064 0.00408 0.00192 0;

0.00408 0.0289 0.0204 0.0119;

0.00192 0.0204 0.0576 0.0336;

0 0.0119 0.0336 0.1225 ];

m = m/12;

C = C/12;

AssetScenarios = mvnrnd(m, C, 20000);

p = PortfolioCVaR('Scenarios', AssetScenarios, ...

'LowerBound', 0, 'LowerBudget', 1, 'UpperBudget', 1, ...

'ProbabilityLevel', 0.95)p =

PortfolioCVaR with properties:

BuyCost: []

SellCost: []

RiskFreeRate: []

ProbabilityLevel: 0.9500

Turnover: []

BuyTurnover: []

SellTurnover: []

NumScenarios: 20000

Name: []

NumAssets: 4

AssetList: []

InitPort: []

AInequality: []

bInequality: []

AEquality: []

bEquality: []

LowerBound: [4×1 double]

UpperBound: []

LowerBudget: 1

UpperBudget: 1

GroupMatrix: []

LowerGroup: []

UpperGroup: []

GroupA: []

GroupB: []

LowerRatio: []

UpperRatio: []

MinNumAssets: []

MaxNumAssets: []

ConditionalBudgetThreshold: []

ConditionalUpperBudget: []

BoundType: []

Note that the LowerBound property value undergoes scalar expansion since AssetScenarios provides the dimensions of the problem.

Using a sequence of steps is an alternative way to accomplish the same task of setting up a “standard” CVaR portfolio optimization problem, given AssetScenarios variable is:

m = [ 0.05; 0.1; 0.12; 0.18 ]; C = [ 0.0064 0.00408 0.00192 0; 0.00408 0.0289 0.0204 0.0119; 0.00192 0.0204 0.0576 0.0336; 0 0.0119 0.0336 0.1225 ]; m = m/12; C = C/12; AssetScenarios = mvnrnd(m, C, 20000); p = PortfolioCVaR; p = setScenarios(p, AssetScenarios); p = PortfolioCVaR(p, 'LowerBound', 0); p = PortfolioCVaR(p, 'LowerBudget', 1, 'UpperBudget', 1); p = setProbabilityLevel(p, 0.95); plotFrontier(p);

This way works because the calls to PortfolioCVaR are in this particular order. In this case, the call to initialize AssetScenarios provides the dimensions for the problem. If you were to do this step last, you would have to explicitly dimension the LowerBound property as follows:

m = [ 0.05; 0.1; 0.12; 0.18 ]; C = [ 0.0064 0.00408 0.00192 0; 0.00408 0.0289 0.0204 0.0119; 0.00192 0.0204 0.0576 0.0336; 0 0.0119 0.0336 0.1225 ]; m = m/12; C = C/12; AssetScenarios = mvnrnd(m, C, 20000); p = PortfolioCVaR; p = PortfolioCVaR(p, 'LowerBound', zeros(size(m))); p = PortfolioCVaR(p, 'LowerBudget', 1, 'UpperBudget', 1); p = setProbabilityLevel(p, 0.95); p = setScenarios(p, AssetScenarios); plotFrontier(p);

If you did not specify the size of LowerBound but, instead, input a scalar argument, the PortfolioCVaR object assumes that you are defining a single-asset problem and produces an error at the call to set asset scenarios with four assets.

You can create a PortfolioCVaR object, p with the PortfolioCVaR object using shortcuts for property names.

m = [ 0.05; 0.1; 0.12; 0.18 ]; C = [ 0.0064 0.00408 0.00192 0; 0.00408 0.0289 0.0204 0.0119; 0.00192 0.0204 0.0576 0.0336; 0 0.0119 0.0336 0.1225 ]; m = m/12; C = C/12; AssetScenarios = mvnrnd(m, C, 20000); p = PortfolioCVaR('scenario', AssetScenarios, 'lb', 0, 'budget', 1, 'plevel', 0.95)

p =

PortfolioCVaR with properties:

BuyCost: []

SellCost: []

RiskFreeRate: []

ProbabilityLevel: 0.9500

Turnover: []

BuyTurnover: []

SellTurnover: []

NumScenarios: 20000

Name: []

NumAssets: 4

AssetList: []

InitPort: []

AInequality: []

bInequality: []

AEquality: []

bEquality: []

LowerBound: [4×1 double]

UpperBound: []

LowerBudget: 1

UpperBudget: 1

GroupMatrix: []

LowerGroup: []

UpperGroup: []

GroupA: []

GroupB: []

LowerRatio: []

UpperRatio: []

MinNumAssets: []

MaxNumAssets: []

ConditionalBudgetThreshold: []

ConditionalUpperBudget: []

BoundType: []

Although not recommended, you can set properties directly, however no error-checking is done on your inputs.

m = [ 0.05; 0.1; 0.12; 0.18 ];

C = [ 0.0064 0.00408 0.00192 0;

0.00408 0.0289 0.0204 0.0119;

0.00192 0.0204 0.0576 0.0336;

0 0.0119 0.0336 0.1225 ];

m = m/12;

C = C/12;

AssetScenarios = mvnrnd(m, C, 20000);

p = PortfolioCVaR;

p = setScenarios(p, AssetScenarios);

p.ProbabilityLevel = 0.95;

p.LowerBudget = 1;

p.UpperBudget = 1;

p.LowerBound = zeros(size(m));

disp(p) PortfolioCVaR with properties:

BuyCost: []

SellCost: []

RiskFreeRate: []

ProbabilityLevel: 0.9500

Turnover: []

BuyTurnover: []

SellTurnover: []

NumScenarios: 20000

Name: []

NumAssets: 4

AssetList: []

InitPort: []

AInequality: []

bInequality: []

AEquality: []

bEquality: []

LowerBound: [4×1 double]

UpperBound: []

LowerBudget: 1

UpperBudget: 1

GroupMatrix: []

LowerGroup: []

UpperGroup: []

GroupA: []

GroupB: []

LowerRatio: []

UpperRatio: []

MinNumAssets: []

MaxNumAssets: []

ConditionalBudgetThreshold: []

ConditionalUpperBudget: []

BoundType: []

Scenarios cannot be assigned directly to a PortfolioCVaR object. Scenarios must always be set through either the PortfolioCVaR function, the setScenarios function, or any of the scenario simulation functions.

Create efficient portfolios:

load CAPMuniverse p = PortfolioCVaR('AssetList',Assets(1:12)); p = simulateNormalScenariosByData(p, Data(:,1:12), 20000 ,'missingdata',true); p = setDefaultConstraints(p); p = setProbabilityLevel(p, 0.95); plotFrontier(p);

pwgt = estimateFrontier(p, 5); pnames = cell(1,5); for i = 1:5 pnames{i} = sprintf('Port%d',i); end Blotter = dataset([{pwgt},pnames],'obsnames',p.AssetList); disp(Blotter);

Port1 Port2 Port3 Port4 Port5

AAPL 0.010223 0.073393 0.11939 0.13137 0

AMZN 0 0 0 0 0

CSCO 0 0 0 0 0

DELL 0.02301 0 0 0 0

EBAY 0 0 0 0 0

GOOG 0.20389 0.38068 0.56253 0.75919 1

HPQ 0.041396 0.009472 0 0 0

IBM 0.44369 0.36472 0.26247 0.10944 0

INTC 0 0 0 0 0

MSFT 0.27779 0.17174 0.055611 0 0

ORCL 0 0 0 0 0

YHOO 0 0 0 0 0

This example shows how to solve a CVaR portfolio optimization problem with constraints in the number of selected assets or conditional (semicontinuous) bounds. To solve this problem, you can use a PortfolioCVaR object along with different mixed integer nonlinear programming (MINLP) solvers.

CVaR Portfolio

Load the returns data in CAPMuniverse.mat. Then, create a PortfolioCVaR object with default constraints and a long-only portfolio whose weights sum to 1. For this example, you can define the feasible region of weights as

% Load data load CAPMuniverse.mat % Create portfolio with default constraints p = PortfolioCVaR(ProbabilityLevel=0.95); p = simulateNormalScenariosByData(p,Data(:,1:12),1000,missingdata=true); p = setDefaultConstraints(p);

Include binary variables for this scenario by setting conditional (semicontinuous) bounds. Conditional bounds are those such that or . In this example, for all assets.

% Set conditional bounds condLB = 0.1; condUB = 0.5; p = setBounds(p,condLB,condUB,BoundType="conditional");

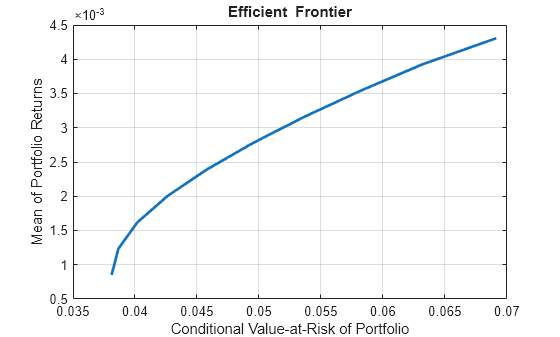

Use estimateFrontier to estimate a set of portfolios on the efficient frontier. The efficient frontier is a curve that shows the trade-off between the return and risk achieved by Pareto-optimal portfolios. For a given return level, the portfolio on the efficient frontier is the one that minimizes the risk while maintaining the desired return. Conversely, for a given risk level, the portfolio on the efficient frontier is the one that maximizes return while maintaining the desired risk level.

% Compute efficient frontier p = setSolverMINLP(p,'TrustRegionCP',DeltaLowerBound=condLB); pwgt = estimateFrontier(p)

pwgt = 12×10

0 0 0 0 0 0 0 0 0 0

0 0 0 0 0 0 0 0 0 0

0 0 0 0 0 0 0 0 0 0

0.1000 0.1090 0.1000 0.1000 0 0 0 0 0 0

0 0 0 0.1000 0.1662 0.2634 0.3369 0.4051 0.4647 0.5000

0.1328 0.2387 0.3331 0.3263 0.3622 0.3543 0.3701 0.3854 0.4287 0.5000

0.1000 0 0 0 0 0 0 0 0 0

0.4132 0.3887 0.2755 0.2552 0.2288 0.1812 0.1110 0 0 0

0 0 0 0 0 0 0 0 0 0

0.2540 0.2636 0.2914 0.2185 0.2427 0.2011 0.1821 0.2095 0.1067 0

0 0 0 0 0 0 0 0 0 0

0 0 0 0 0 0 0 0 0 0

% Compute risk and returns of the portfolios on the efficient frontier

rsk = estimatePortRisk(p,pwgt)rsk = 10×1

0.0368

0.0377

0.0398

0.0423

0.0453

0.0485

0.0520

0.0558

0.0598

0.0647

ret = estimatePortReturn(p,pwgt)

ret = 10×1

0.0009

0.0012

0.0014

0.0016

0.0019

0.0021

0.0023

0.0026

0.0028

0.0030

Plot the weights from the frontier estimation using plotFrontier. The resulting curve is piece-wise concave with possible vertical jumps (discontinuities) between the concave intervals.

% Plot efficient frontier

plotFrontier(p,pwgt)

Changing MINLP Solvers

In the previous section, you use the default solver for estimateFrontier. However, you can solve mixed-integer portfolio problems using any of the three algorithms supported by setSolverMINLP: OuterApproximation, ExtendedCP, and TrustRegionCP. Furthermore, the OuterApproximation algorithm accepts an additional name-value argument (ExtendedFormulation) for Portfolio problems, which reformulates problems with quadratic functions to work in an extended space that usually decreases the computation time. All algorithms, including the extended formulation variation of the OuterApproximation algorithm, return the same values within numerical accuracy. The available solvers are:

OuterApproximation— The default algorithm, which is robust and usually faster thanExtenedCPOuterApproximationwithExtendedFormulationset totrue— A robust algorithm that is usually faster than other algorithms, but only supported forPortfolioobject problemsExtendedCP— The most robust solver, but usually the slowestTrustRegionCP— The fastest algorithm, but one that is less robust and may provide suboptimal solutions

For more information on solvers for mixed-integer portfolio problems, see Choose MINLP Solvers for Portfolio Problems.

To change the MINLP solvers, use setSolverMINLP.

% Select 'TrustRegionCP' as solver p_OA = setSolverMINLP(p,'OuterApproximation'); pwgt_OA = estimateFrontier(p_OA); rskOA = estimatePortRisk(p,pwgt_OA); retOA = estimatePortReturn(p,pwgt_OA); % Select 'ExtendedCP' as solver using 'midway' cuts as 'CutGeneration' p_ECP = setSolverMINLP(p,'ExtendedCP',CutGeneration="midway"); pwgt_ECP = estimateFrontier(p_ECP); rskECP = estimatePortRisk(p,pwgt_ECP); retECP = estimatePortReturn(p,pwgt_ECP);

Compare the returns and risks obtained by the portfolios on the efficient frontier from the different solvers. They are all the same within a numerical accuracy that is an absolute difference .

retTable = table(retOA,ret,retECP,'VariableNames',{'OA','TR','ECP'})

retTable=10×3 table

OA TR ECP

__________ __________ __________

0.00092881 0.00092876 0.00092876

0.0011614 0.0011613 0.0011613

0.001394 0.0013939 0.0013939

0.0016265 0.0016265 0.0016265

0.0018591 0.0018591 0.0018591

0.0020917 0.0020917 0.0020917

0.0023243 0.0023243 0.0023243

0.0025569 0.0025569 0.0025569

0.0027894 0.0027894 0.0027894

0.003022 0.003022 0.003022

rskTable = table(rskOA,rsk,rskECP,'VariableNames',{'OA','TR','ECP'})

rskTable=10×3 table

OA TR ECP

________ ________ ________

0.036808 0.036808 0.036808

0.037658 0.037658 0.037658

0.039808 0.039808 0.039808

0.042256 0.042256 0.042256

0.04527 0.045269 0.045269

0.048489 0.048488 0.048488

0.051963 0.051963 0.051963

0.055783 0.055783 0.055783

0.059828 0.059828 0.059828

0.064705 0.064705 0.064705

% Compare risks from the different OuterApproximation formulations

norm(rskTable.OA-rskTable.TR,Inf) <= 1e-4ans = logical

1

More About

References

[1] For a complete list of references for the PortfolioCVaR object, see Portfolio Optimization.

Version History

Introduced in R2012bSee Also

plotFrontier | estimateFrontier | setScenarios | Portfolio | PortfolioMAD | nearcorr

Topics

- Creating the PortfolioCVaR Object

- Common Operations on the PortfolioCVaR Object

- Working with CVaR Portfolio Constraints Using Defaults

- Asset Returns and Scenarios Using PortfolioCVaR Object

- Estimate Efficient Portfolios for Entire Frontier for PortfolioCVaR Object

- Estimate Efficient Frontiers for PortfolioCVaR Object

- Postprocessing Results to Set Up Tradable Portfolios

- Hedging Using CVaR Portfolio Optimization

- Bond Portfolio CVaR Optimization Using Diebold-Li Model

- Portfolio Optimization Theory

- PortfolioCVaR Object Workflow

- PortfolioCVaR Object Properties and Functions

- Working with PortfolioCVaR Objects

- Setting and Getting Properties

- Displaying PortfolioCVaR Objects

- Saving and Loading PortfolioCVaR Objects

- Estimating Efficient Portfolios and Frontiers

- Arrays of PortfolioCVaR Objects

- Subclassing PortfolioCVaR Objects

- Conventions for Representation of Data

- Supported Constraints for Portfolio Optimization Using PortfolioCVaR Object

- Adding Constraints to Satisfy UCITS Directive

- Choosing and Controlling the Solver for PortfolioCVaR Optimizations

- Choose MINLP Solvers for Portfolio Problems