infer

Infer univariate ARIMA or ARIMAX model residuals or conditional variances

Syntax

Description

Tbl2 = infer(Mdl,Tbl1)Tbl2 containing paths of

residuals and conditional variances inferred from the model

Mdl and the response data in the input table or

timetable Tbl1. (since R2023b)

infer selects the response variable named in

Mdl.SeriesName or the sole variable in

Tbl1. To select a different response variable in

Tbl1 to infer residuals and conditional variances, use

the ResponseVariable name-value argument.

[___] = infer(___,

specifies options using one or more name-value arguments in

addition to any of the input argument combinations in previous syntaxes.

Name=Value)infer returns the output argument combination for the

corresponding input arguments. For example, infer(Mdl,Y,Y0=PS,X=Pred) infers

residuals from the numeric vector of responses Y with

respect to the ARIMAX Mdl, and specifies the numeric vector

of presample response data PS to initialize the model and the

exogenous predictor data Pred for the regression

component.

Examples

Infer residuals from an AR model by supplying a hypothetical response series in a vector.

Specify an AR(2) model using known parameters.

Mdl = arima(AR={0.5 -0.8},Constant=0.002, ...

Variance=0.8);Simulate response data with 100 observations.

rng(1,"twister");

Y = simulate(Mdl,100);Y is a 100-by-1 vector containing a random response path drawn from Mdl.

Infer residuals for all corresponding responses.

E = infer(Mdl,Y);

E is a 100-by-1 vector containing a residuals corresponding to Y, with respect to Mdl. By default, infer backcasts for required presample observations.

Plot the residuals.

figure

plot(E)

title("Inferred Residuals")

Infer the conditional variances from an AR(1) and GARCH(1,1) composite model. Return the loglikelihood value.

Specify an AR(1) model using known parameters. Set the variance equal to a garch model.

Mdl = arima(AR={0.8 -0.3},Constant=0);

MdlVar = garch(Constant=0.0002,GARCH=0.6,ARCH=0.2);

Mdl.Variance = MdlVar;Simulate response data with 100 observations.

rng(1,"twister")

Y = simulate(Mdl,100);Infer residuals and conditional variances for the entire response series. Compute the loglikelihood at the simulated data.

[E,V,logL] = infer(Mdl,Y); logL

logL = 209.6405

E and V are 100-by-1 vectors of inferred residuals and conditional variances, given the response data and model.

Plot the conditional variances.

figure

plot(V)

title("Inferred Conditional Variances")

Infer residuals from an AR model by supplying a hypothetical response series in a vector. Supply presample responses to initialize the model.

Specify an AR(2) model using known parameters.

Mdl = arima(AR={0.5 -0.8},Constant=0.002, ...

Variance=0.8)Mdl =

arima with properties:

Description: "ARIMA(2,0,0) Model (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

P: 2

D: 0

Q: 0

Constant: 0.002

AR: {0.5 -0.8} at lags [1 2]

SAR: {}

MA: {}

SMA: {}

Seasonality: 0

Beta: [1×0]

Variance: 0.8

Consider inferring residuals from a response series of length T = 100. Because the model requires Mdl.P responses to initialize the model, simulate T + Mdl.P = 102 responses from the model.

rng(1,"twister");

T = 100;

TSim = T + Mdl.P;

y = simulate(Mdl,TSim);Y is a 102-by-1 vector representing a random response path drawn from the model.

Infer residuals from the last T response and use the first Mdl.P observations as a presample to initialize the model.

E = infer(Mdl,y((Mdl.P+1):end),Y0=y(1:Mdl.P)); size(E)

ans = 1×2

100 1

E is a 100-by-1 vector containing a residuals corresponding to the last 100 observations of y, with respect to Mdl.

Plot the residuals.

figure

plot(E)

title("Inferred Residuals")

Since R2023b

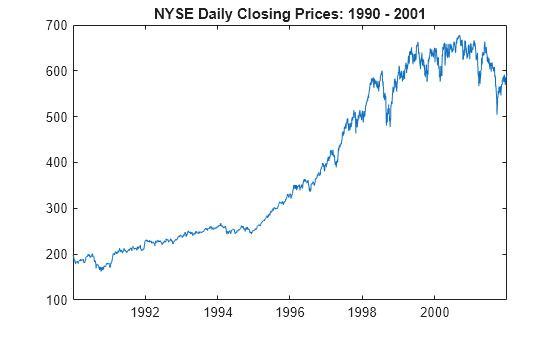

Fit an ARIMA(1,1,1) model to the weekly average NYSE closing prices. Supply timetables of in-sample and presample data for the fit. Then, infer the residuals from the fit.

Load Data

Load the US equity index data set Data_EquityIdx.

load Data_EquityIdx

T = height(DataTimeTable)T = 3028

The timetable DataTimeTable includes the time series variable NYSE, which contains daily NYSE composite closing prices from January 1990 through December 2001.

Plot the daily NYSE price series.

figure

plot(DataTimeTable.Time,DataTimeTable.NYSE)

title("NYSE Daily Closing Prices: 1990 - 2001")

Prepare Timetable for Estimation

When you plan to supply a timetable, you must ensure it has all the following characteristics:

The selected response variable is numeric and does not contain any missing values.

The timestamps in the

Timevariable are regular, and they are ascending or descending.

Remove all missing values from the timetable, relative to the NYSE price series.

DTT = rmmissing(DataTimeTable,DataVariables="NYSE");

T_DTT = height(DTT)T_DTT = 3028

Because all sample times have observed NYSE prices, rmmissing does not remove any observations.

Determine whether the sampling timestamps have a regular frequency and are sorted.

areTimestampsRegular = isregular(DTT,"days")areTimestampsRegular = logical

0

areTimestampsSorted = issorted(DTT.Time)

areTimestampsSorted = logical

1

areTimestampsRegular = 0 indicates that the timestamps of DTT are irregular. areTimestampsSorted = 1 indicates that the timestamps are sorted. Business day rules make daily macroeconomic measurements irregular.

Remedy the time irregularity by computing the weekly average closing price series of all timetable variables.

DTTW = convert2weekly(DTT,Aggregation="mean"); areTimestampsRegular = isregular(DTTW,"weeks")

areTimestampsRegular = logical

1

T_DTTW = height(DTTW)

T_DTTW = 627

DTTW is regular.

figure

plot(DTTW.Time,DTTW.NYSE)

title("NYSE Daily Closing Prices: 1990 - 2001")

Create Model Template for Estimation

Suppose that an ARIMA(1,1,1) model is appropriate to model NYSE composite series during the sample period.

Create an ARIMA(1,1,1) model template for estimation.

Mdl = arima(1,1,1);

Mdl is a partially specified arima model object.

Fit Model to Data

infer requires Mdl.P presample observations to initialize the model. infer backcasts for necessary presample responses, but you can provide a presample.

Partition the data into presample and in-sample, or estimation sample, observations.

T0 = Mdl.P; DTTW0 = DTTW(1:T0,:); DTTW1 = DTTW((T0+1):end,:);

Fit an ARIMA(1,1,1) model to the in-sample weekly average NYSE closing prices. Specify the response variable name, presample timetable, and the presample response variable name.

EstMdl = estimate(Mdl,DTTW1,ResponseVariable="NYSE", ... Presample=DTTW0,PresampleResponseVariable="NYSE");

ARIMA(1,1,1) Model (Gaussian Distribution):

Value StandardError TStatistic PValue

________ _____________ __________ ___________

Constant 0.83623 0.453 1.846 0.064892

AR{1} -0.32862 0.23526 -1.3968 0.16247

MA{1} 0.42703 0.22613 1.8884 0.058967

Variance 56.065 1.8433 30.416 3.3798e-203

EstMdl is a fully specified, estimated arima model object.

Infer Residuals

Infer the residuals from the fitted model and in-sample observations. Specify the response variable name, presample timetable, and the presample response variable name.

Tbl2 = infer(EstMdl,DTTW1,ResponseVariable="NYSE", ... Presample=DTTW0,PresampleResponseVariable="NYSE"); tail(Tbl2)

Time NYSE NASDAQ Y_Residual Y_Variance

___________ ______ ______ __________ __________

16-Nov-2001 577.11 1886.9 5.8649 56.065

23-Nov-2001 583 1898.3 5.3303 56.065

30-Nov-2001 581.41 1925.8 -2.7678 56.065

07-Dec-2001 584.96 1998.1 3.3787 56.065

14-Dec-2001 574.03 1981 -12.038 56.065

21-Dec-2001 582.1 1967.9 8.7774 56.065

28-Dec-2001 590.28 1967.2 6.2526 56.065

04-Jan-2002 589.8 1950.4 -1.3008 56.065

size(Tbl2)

ans = 1×2

625 4

Tbl2 is a 625-by-4 timetable containing all variables in DTTW1, and the inferred residuals from the fit NYSE_Response and constant variance paths NYSE_Variance (Mdl.Variance = 56.065).

Since R2023b

Fit an ARIMA(1,1,1) model to the weekly average NYSE closing prices. Supply a timetable of data and specify the series for the fit. Then, compute fitted responses.

Load the US equity index data set Data_EquityIdx.

load Data_EquityIdx

T = height(DataTimeTable)T = 3028

Remedy the time irregularity by computing the weekly average closing price series of all timetable variables.

DTTW = convert2weekly(DataTimeTable,Aggregation="mean");

T_DTTW = height(DTTW)T_DTTW = 627

Create an ARIMA(1,1,1) model template for estimation. Set the response series name to NYSE.

Mdl = arima(1,1,1);

Mdl.SeriesName = "NYSE";Partition the data into presample and in-sample, or estimation sample, observations.

T0 = Mdl.P; DTTW0 = DTTW(1:T0,:); DTTW1 = DTTW((T0+1):end,:);

Fit an ARIMA(1,1,1) model to the in-sample weekly average NYSE closing prices. Specify the presample timetable, and the presample response variable name.

EstMdl = estimate(Mdl,DTTW1,Presample=DTTW0, ... PresampleResponseVariable="NYSE");

ARIMA(1,1,1) Model (Gaussian Distribution):

Value StandardError TStatistic PValue

________ _____________ __________ ___________

Constant 0.83623 0.453 1.846 0.064891

AR{1} -0.32862 0.23526 -1.3968 0.16247

MA{1} 0.42703 0.22613 1.8884 0.058966

Variance 56.065 1.8433 30.416 3.3799e-203

Infer the residuals from the fitted model and in-sample observations. Specify the presample timetable, and the presample response variable name.

Tbl2 = infer(EstMdl,DTTW1,Presample=DTTW0, ... PresampleResponseVariable="NYSE");

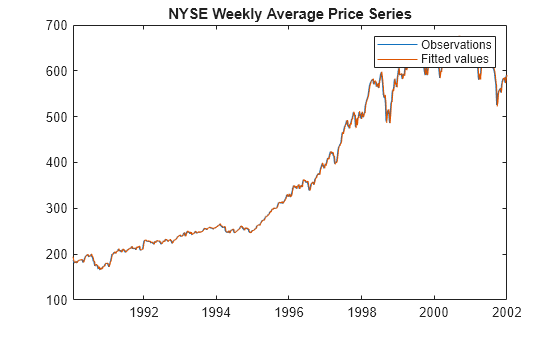

Compute fitted response values by subtracting the residuals from the observed response series.

Tbl2.YHat = Tbl2.NYSE - Tbl2.NYSE_Residual;

Plot the observed responses and the fitted values.

figure plot(Tbl2.Time,[Tbl2.NYSE Tbl2.YHat]) legend("Observations","Fitted values") title("NYSE Weekly Average Price Series")

The fitted values closely track the observations.

Plot the residuals versus the fitted values.

figure plot(Tbl2.YHat,Tbl2.NYSE_Residual,".",MarkerSize=15) ylabel("Residuals") xlabel("Fitted Values") title("Residual Plot")

Residual variance appears larger for larger fitted values. One remedy for this behavior is to apply the log transform to the data.

Infer residuals from an ARMAX model.

Specify an ARMA(1,2) model using known parameters for the response (MdlY) and an AR(1) model for the predictor data (MdlX).

MdlY = arima(AR=0.2,MA={-0.1,0.6},Constant=1, ...

Variance=2,Beta=3)MdlY =

arima with properties:

Description: "ARIMAX(1,0,2) Model (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

P: 1

D: 0

Q: 2

Constant: 1

AR: {0.2} at lag [1]

SAR: {}

MA: {-0.1 0.6} at lags [1 2]

SMA: {}

Seasonality: 0

Beta: [3]

Variance: 2

MdlX = arima(AR=0.3,Constant=0,Variance=1);

If you do not specify presample responses, infer requires at least T + MdlY.P predictor observations to simulate a response series of length T.

Consider simulating a response series of length 100. Simulate a predictor series of length 101, and then simulate the response series. Provide the predictor data to simulate for the exogenous regression component.

rng(1,"twister") % For reproducibility T = 100; Pred = simulate(MdlX,T + MdlY.P); Y = simulate(MdlY,T,X=Pred);

Infer residuals using the entire series.

E = infer(MdlY,Y,X=Pred);

figure

plot(E)

title("Inferred Residuals")

Input Arguments

Name-Value Arguments

Output Arguments

Algorithms

If you supply data in the table or timetable Tbl1 to estimate an

ARIMAX model, infer cannot backcast for presample responses.

Therefore, if you specify PredictorVariables, you must also specify

presample response data by using the Presample and

PresampleResponseVariable name-value arguments.

References

[1] Box, G. E. P., G. M. Jenkins, and G. C. Reinsel. Time Series Analysis: Forecasting and Control 3rd ed. Englewood Cliffs, NJ: Prentice Hall, 1994.

[2] Enders, W. Applied Econometric Time Series. Hoboken, NJ: John Wiley & Sons, 1995.

[3] Hamilton, J. D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.