incrementalLearner

Convert support vector machine (SVM) regression model to incremental learner

Description

IncrementalMdl = incrementalLearner(Mdl)IncrementalMdl, using the hyperparameters and coefficients of the traditionally trained linear SVM model for regression, Mdl. Because its property values reflect the knowledge gained from Mdl, IncrementalMdl can predict labels given new observations, and it is warm, meaning that its predictive performance is tracked.

IncrementalMdl = incrementalLearner(Mdl,Name,Value)IncrementalMdl before its

predictive performance is tracked. For example,

'MetricsWarmupPeriod',50,'MetricsWindowSize',100 specifies a preliminary

incremental training period of 50 observations before performance metrics are tracked, and

specifies processing 100 observations before updating the window performance metrics.

Examples

Train an SVM regression model by using fitrsvm, and then convert it to an incremental learner.

Load and Preprocess Data

Load the 2015 NYC housing data set. For more details on the data, see NYC Open Data.

load NYCHousing2015Extract the response variable SALEPRICE from the table. For numerical stability, scale SALEPRICE by 1e6.

Y = NYCHousing2015.SALEPRICE/1e6; NYCHousing2015.SALEPRICE = [];

Create dummy variable matrices from the categorical predictors.

catvars = ["BOROUGH" "BUILDINGCLASSCATEGORY" "NEIGHBORHOOD"]; dumvarstbl = varfun(@(x)dummyvar(categorical(x)),NYCHousing2015,... 'InputVariables',catvars); dumvarmat = table2array(dumvarstbl); NYCHousing2015(:,catvars) = [];

Treat all other numeric variables in the table as linear predictors of sales price. Concatenate the matrix of dummy variables to the rest of the predictor data.

idxnum = varfun(@isnumeric,NYCHousing2015,'OutputFormat','uniform')

idxnum = 1×6 logical array

1 1 1 1 1 0

X = [dumvarmat NYCHousing2015{:,idxnum}];Train SVM Regression Model

Fit an SVM regression model to 5000 randomly drawn observations from the data set. Discard the support vectors (Alpha) from the model so that the software uses linear coefficients (Beta) for prediction.

N = numel(Y);

n = 5000;

rng(1); % For reproducibility

idx = randsample(N,n);

TTMdl = fitrsvm(X(idx,:),Y(idx));

TTMdl = discardSupportVectors(TTMdl)TTMdl =

RegressionSVM

ResponseName: 'Y'

CategoricalPredictors: []

ResponseTransform: 'none'

Beta: [312×1 double]

Bias: 64.5811

KernelParameters: [1×1 struct]

NumObservations: 5000

BoxConstraints: [5000×1 double]

ConvergenceInfo: [1×1 struct]

IsSupportVector: [5000×1 logical]

Solver: 'SMO'

Properties, Methods

TTMdl is a RegressionSVM model object representing a traditionally trained SVM regression model.

Convert Trained Model

Convert the traditionally trained SVM regression model to a linear regression model for incremental learning.

IncrementalMdl = incrementalLearner(TTMdl)

IncrementalMdl =

incrementalRegressionLinear

IsWarm: 1

Metrics: [1×2 table]

ResponseTransform: 'none'

Beta: [312×1 double]

Bias: 64.5811

Learner: 'svm'

Properties, Methods

IncrementalMdl is an incrementalRegressionLinear model object prepared for incremental learning using SVM.

The

incrementalLearnerfunction initializes the incremental learner by passing learned coefficients to it, along with other informationTTMdlextracted from the training data.IncrementalMdlis warm (IsWarmis1), which means that incremental learning functions can start tracking performance metrics.The

incrementalLearnerfunction trains the model using the adaptive scale-invariant solver, whereasfitrsvmtrainedTTMdlusing the SMO solver.

Predict Responses

An incremental learner created from converting a traditionally trained model can generate predictions without further processing.

Predict sales prices for all observations using both models.

ttyfit = predict(TTMdl,X); ilyfit = predict(IncrementalMdl,X); compareyfit = norm(ttyfit - ilyfit)

compareyfit = 0

The difference between the fitted values generated by the models is 0.

The default solver is the adaptive scale-invariant solver. If you specify this solver, you do not need to tune any parameters for training. However, if you specify either the standard SGD or ASGD solver instead, you can also specify an estimation period, during which the incremental fitting functions tune the learning rate.

Load and shuffle the 2015 NYC housing data set. For more details on the data, see NYC Open Data.

load NYCHousing2015 rng(1) % For reproducibility n = size(NYCHousing2015,1); shuffidx = randsample(n,n); NYCHousing2015 = NYCHousing2015(shuffidx,:);

Extract the response variable SALEPRICE from the table. For numerical stability, scale SALEPRICE by 1e6.

Y = NYCHousing2015.SALEPRICE/1e6; NYCHousing2015.SALEPRICE = [];

Create dummy variable matrices from the categorical predictors.

catvars = ["BOROUGH" "BUILDINGCLASSCATEGORY" "NEIGHBORHOOD"]; dumvarstbl = varfun(@(x)dummyvar(categorical(x)),NYCHousing2015,... 'InputVariables',catvars); dumvarmat = table2array(dumvarstbl); NYCHousing2015(:,catvars) = [];

Treat all other numeric variables in the table as linear predictors of sales price. Concatenate the matrix of dummy variables to the rest of the predictor data.

idxnum = varfun(@isnumeric,NYCHousing2015,'OutputFormat','uniform'); X = [dumvarmat NYCHousing2015{:,idxnum}];

Randomly partition the data into 5% and 95% sets: the first set for training a model traditionally, and the second set for incremental learning.

cvp = cvpartition(n,'Holdout',0.95); idxtt = training(cvp); idxil = test(cvp); % 5% set for traditional training Xtt = X(idxtt,:); Ytt = Y(idxtt); % 95% set for incremental learning Xil = X(idxil,:); Yil = Y(idxil);

Fit an SVM regression model to 5% of the data.

TTMdl = fitrsvm(Xtt,Ytt);

Convert the traditionally trained SVM regression model to a linear regression model for incremental learning. Specify the standard SGD solver and an estimation period of 2e4 observations (the default is 1000 when a learning rate is required).

IncrementalMdl = incrementalLearner(TTMdl,'Solver','sgd','EstimationPeriod',2e4);

IncrementalMdl is an incrementalRegressionLinear model object.

Fit the incremental model to the rest of the data by using the fit function. At each iteration:

Simulate a data stream by processing 10 observations at a time.

Overwrite the previous incremental model with a new one fitted to the incoming observations.

Store the initial learning rate and to see how the coefficients and rate evolve during training.

% Preallocation nil = numel(Yil); numObsPerChunk = 10; nchunk = floor(nil/numObsPerChunk); learnrate = [IncrementalMdl.LearnRate; zeros(nchunk,1)]; beta1 = [IncrementalMdl.Beta(1); zeros(nchunk,1)]; % Incremental fitting for j = 1:nchunk ibegin = min(nil,numObsPerChunk*(j-1) + 1); iend = min(nil,numObsPerChunk*j); idx = ibegin:iend; IncrementalMdl = fit(IncrementalMdl,Xil(idx,:),Yil(idx)); beta1(j + 1) = IncrementalMdl.Beta(1); learnrate(j + 1) = IncrementalMdl.LearnRate; end

IncrementalMdl is an incrementalRegressionLinear model object trained on all the data in the stream.

To see how the initial learning rate and evolve during training, plot them on separate tiles.

t = tiledlayout(2,1); nexttile plot(beta1) hold on ylabel('\beta_1') xline(IncrementalMdl.EstimationPeriod/numObsPerChunk,'r-.') nexttile plot(learnrate) ylabel('Initial Learning Rate') xline(IncrementalMdl.EstimationPeriod/numObsPerChunk,'r-.') xlabel(t,'Iteration')

The initial learning rate jumps from 0.7 to its autotuned value after the estimation period. During training, the software uses a learning rate that gradually decays from the initial value specified in the LearnRateSchedule property of IncrementalMdl.

Because fit does not fit the model to the streaming data during the estimation period, is constant for the first 2000 iterations (20,000 observations). Then, changes slightly as fit fits the model to each new chunk of 10 observations.

Use a trained SVM regression model to initialize an incremental learner. Prepare the incremental learner by specifying a metrics warm-up period, during which the updateMetricsAndFit function only fits the model. Specify a metrics window size of 500 observations.

Load the robot arm data set.

load robotarmFor details on the data set, enter Description at the command line.

Randomly partition the data into 5% and 95% sets: the first set for training a model traditionally, and the second set for incremental learning.

n = numel(ytrain); rng(1) % For reproducibility cvp = cvpartition(n,'Holdout',0.95); idxtt = training(cvp); idxil = test(cvp); % 5% set for traditional training Xtt = Xtrain(idxtt,:); Ytt = ytrain(idxtt); % 95% set for incremental learning Xil = Xtrain(idxil,:); Yil = ytrain(idxil);

Fit an SVM regression model to the first set.

TTMdl = fitrsvm(Xtt,Ytt);

Convert the traditionally trained SVM regression model to a linear regression model for incremental learning. Specify the following:

A performance metrics warm-up period of 2000 observations.

A metrics window size of 500 observations.

Use of epsilon insensitive loss, MSE, and mean absolute error (MAE) to measure the performance of the model. The software supports epsilon insensitive loss and MSE. Create an anonymous function that measures the absolute error of each new observation. Create a structure array containing the name

MeanAbsoluteErrorand its corresponding function.

maefcn = @(z,zfit)abs(z - zfit); maemetric = struct("MeanAbsoluteError",maefcn); IncrementalMdl = incrementalLearner(TTMdl,'MetricsWarmupPeriod',2000,'MetricsWindowSize',500,... 'Metrics',{'epsiloninsensitive' 'mse' maemetric});

Fit the incremental model to the rest of the data by using the updateMetricsAndFit function. At each iteration:

Simulate a data stream by processing 50 observations at a time.

Overwrite the previous incremental model with a new one fitted to the incoming observations.

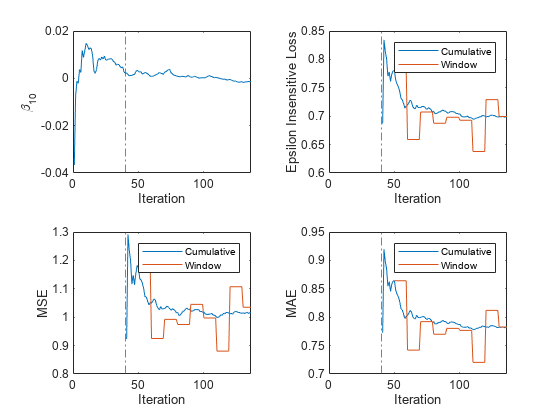

Store the estimated coefficient , the cumulative metrics, and the window metrics to see how they evolve during incremental learning.

% Preallocation nil = numel(Yil); numObsPerChunk = 50; nchunk = floor(nil/numObsPerChunk); ei = array2table(zeros(nchunk,2),'VariableNames',["Cumulative" "Window"]); mse = array2table(zeros(nchunk,2),'VariableNames',["Cumulative" "Window"]); mae = array2table(zeros(nchunk,2),'VariableNames',["Cumulative" "Window"]); beta1 = [IncrementalMdl.Beta(10); zeros(nchunk,1)]; % Incremental fitting for j = 1:nchunk ibegin = min(nil,numObsPerChunk*(j-1) + 1); iend = min(nil,numObsPerChunk*j); idx = ibegin:iend; IncrementalMdl = updateMetricsAndFit(IncrementalMdl,Xil(idx,:),Yil(idx)); ei{j,:} = IncrementalMdl.Metrics{"EpsilonInsensitiveLoss",:}; mse{j,:} = IncrementalMdl.Metrics{"MeanSquaredError",:}; mae{j,:} = IncrementalMdl.Metrics{"MeanAbsoluteError",:}; beta1(j + 1) = IncrementalMdl.Beta(10); end

IncrementalMdl is an incrementalRegressionLinear model object trained on all the data in the stream. During incremental learning and after the model is warmed up, updateMetricsAndFit checks the performance of the model on the incoming observations, and then fits the model to those observations.

To see how the performance metrics and evolve during training, plot them on separate tiles.

tiledlayout(2,2) nexttile plot(beta1) ylabel('\beta_{10}') xlim([0 nchunk]) xline(IncrementalMdl.MetricsWarmupPeriod/numObsPerChunk,'r-.') xlabel('Iteration') nexttile h = plot(ei.Variables); xlim([0 nchunk]) ylabel('Epsilon Insensitive Loss') xline(IncrementalMdl.MetricsWarmupPeriod/numObsPerChunk,'r-.') legend(h,ei.Properties.VariableNames) xlabel('Iteration') nexttile h = plot(mse.Variables); xlim([0 nchunk]) ylabel('MSE') xline(IncrementalMdl.MetricsWarmupPeriod/numObsPerChunk,'r-.') legend(h,mse.Properties.VariableNames) xlabel('Iteration') nexttile h = plot(mae.Variables); xlim([0 nchunk]) ylabel('MAE') xline(IncrementalMdl.MetricsWarmupPeriod/numObsPerChunk,'r-.') legend(h,mae.Properties.VariableNames) xlabel('Iteration')

The plot suggests that updateMetricsAndFit does the following:

Fit during all incremental learning iterations.

Compute the performance metrics after the metrics warm-up period only.

Compute the cumulative metrics during each iteration.

Compute the window metrics after processing 500 observations.

Input Arguments

Name-Value Arguments

Output Arguments

More About

Algorithms

References

Version History

Introduced in R2020b