Logistic

Create Logistic model object for lifetime probability of

default

Description

Create and analyze a Logistic model object to calculate

the lifetime probability (PD) of default using this workflow:

Use

fitLifetimePDModelto create aLogisticmodel object.Use

predictto predict the conditional PD andpredictLifetimeto predict the lifetime PD.Use

modelDiscriminationto return AUROC and ROC data. You can plot the results usingmodelDiscriminationPlot.Use

modelCalibrationto return the RMSE of the observed and predicted PD data. You can plot the results usingmodelCalibrationPlot.

Creation

Syntax

Description

LogisticPDModel = fitLifetimePDModel(data,ModelType)Logistic PD model object.

If you do not specify variable information for

IDVar, AgeVar,

LoanVars, MacroVars, and

ResponseVar, then:

IDVaris set to the first column in thedatainput.LoanVarsis set to include all columns from the second to the second-to-last columns of thedatainput.ResponseVaris set to the last column in thedatainput.

LogisticPDModel = fitLifetimePDModel(___,Name,Value)LogisticPDModel =

fitLifetimePDModel(data(TrainDataInd,:),"Logistic",ModelID="Logistic_A",Description="Logisitic_model",AgeVar="YOB",IDVar="ID",LoanVars="ScoreGroup",MacroVars={'GDP','Market'},ResponseVar="Default",WeightsVar="Weights")

creates a LogisticPDModel object using a

Logistic model type.

Input Arguments

Name-Value Arguments

Properties

Object Functions

predict | Compute conditional PD |

predictLifetime | Compute cumulative lifetime PD, marginal PD, and survival probability |

modelDiscrimination | Compute AUROC and ROC data |

modelCalibration | Compute RMSE of predicted and observed PDs on grouped data |

modelDiscriminationPlot | Plot ROC curve |

modelCalibrationPlot | Plot observed default rates compared to predicted PDs on grouped data |

Examples

This example shows how to use fitLifetimePDModel to create a Logistic model using credit and macroeconomic data.

Load Data

Load the credit portfolio data.

load RetailCreditPanelData.mat

disp(head(data)) ID ScoreGroup YOB Default Year

__ __________ ___ _______ ____

1 Low Risk 1 0 1997

1 Low Risk 2 0 1998

1 Low Risk 3 0 1999

1 Low Risk 4 0 2000

1 Low Risk 5 0 2001

1 Low Risk 6 0 2002

1 Low Risk 7 0 2003

1 Low Risk 8 0 2004

disp(head(dataMacro))

Year GDP Market

____ _____ ______

1997 2.72 7.61

1998 3.57 26.24

1999 2.86 18.1

2000 2.43 3.19

2001 1.26 -10.51

2002 -0.59 -22.95

2003 0.63 2.78

2004 1.85 9.48

Join the two data components into a single data set.

data = join(data,dataMacro); disp(head(data))

ID ScoreGroup YOB Default Year GDP Market

__ __________ ___ _______ ____ _____ ______

1 Low Risk 1 0 1997 2.72 7.61

1 Low Risk 2 0 1998 3.57 26.24

1 Low Risk 3 0 1999 2.86 18.1

1 Low Risk 4 0 2000 2.43 3.19

1 Low Risk 5 0 2001 1.26 -10.51

1 Low Risk 6 0 2002 -0.59 -22.95

1 Low Risk 7 0 2003 0.63 2.78

1 Low Risk 8 0 2004 1.85 9.48

Partition Data

Separate the data into training and test partitions.

nIDs = max(data.ID); uniqueIDs = unique(data.ID); rng('default'); % for reproducibility c = cvpartition(nIDs,'HoldOut',0.4); TrainIDInd = training(c); TestIDInd = test(c); TrainDataInd = ismember(data.ID,uniqueIDs(TrainIDInd)); TestDataInd = ismember(data.ID,uniqueIDs(TestIDInd));

Create Logistic Lifetime PD Model

Use fitLifetimePDModel to create a Logistic model using the training data.

pdModel = fitLifetimePDModel(data(TrainDataInd,:),"Logistic",... 'AgeVar','YOB',... 'IDVar','ID',... 'LoanVars','ScoreGroup',... 'MacroVars',{'GDP','Market'},... 'ResponseVar','Default'); disp(pdModel)

Logistic with properties:

ModelID: "Logistic"

Description: ""

UnderlyingModel: [1×1 classreg.regr.CompactGeneralizedLinearModel]

IDVar: "ID"

AgeVar: "YOB"

LoanVars: "ScoreGroup"

MacroVars: ["GDP" "Market"]

ResponseVar: "Default"

WeightsVar: ""

TimeInterval: 1

Display the underlying model.

pdModel.UnderlyingModel

ans =

Compact generalized linear regression model:

logit(Default) ~ 1 + ScoreGroup + YOB + GDP + Market

Distribution = Binomial

Estimated Coefficients:

Estimate SE tStat pValue

__________ _________ _______ ___________

(Intercept) -2.7422 0.10136 -27.054 3.408e-161

ScoreGroup_Medium Risk -0.68968 0.037286 -18.497 2.1894e-76

ScoreGroup_Low Risk -1.2587 0.045451 -27.693 8.4736e-169

YOB -0.30894 0.013587 -22.738 1.8738e-114

GDP -0.11111 0.039673 -2.8006 0.0051008

Market -0.0083659 0.0028358 -2.9502 0.0031761

388097 observations, 388091 error degrees of freedom

Dispersion: 1

Chi^2-statistic vs. constant model: 1.85e+03, p-value = 0

Predict Conditional and Lifetime PD

Use the predict function to predict conditional PD values. The prediction is a row-by-row prediction.

dataCustomer1 = data(1:8,:); CondPD = predict(pdModel,dataCustomer1)

CondPD = 8×1

0.0092

0.0053

0.0045

0.0039

0.0037

0.0037

0.0019

0.0012

Use predictLifetime to predict the lifetime cumulative PD values (computing marginal and survival PD values is also supported). The predictLifetime function uses the ID variable (see the 'IDVar' property for the Logistic object) to transform conditional PDs to cumulative PDs for each ID.

LifetimePD = predictLifetime(pdModel,dataCustomer1)

LifetimePD = 8×1

0.0092

0.0145

0.0189

0.0228

0.0264

0.0300

0.0319

0.0330

Validate Model

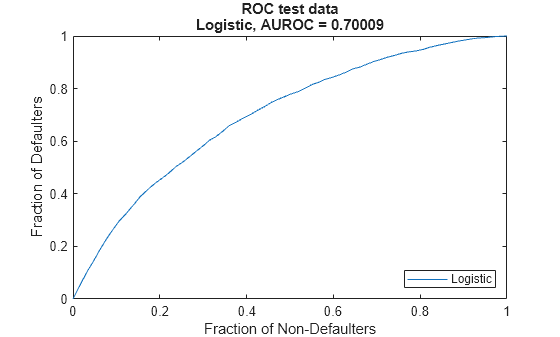

Use modelDiscrimination to measure the ranking of customers by PD.

DiscMeasure = modelDiscrimination(pdModel,data(TestDataInd,:),DataID='test data');

disp(DiscMeasure) AUROC

_______

Logistic, test data 0.70009

Use modelDiscriminationPlot to visualize the ROC curve.

modelDiscriminationPlot(pdModel,data(TestDataInd,:),DataID='test data');

Use modelCalibration to measure the calibration of the predicted PD values. The modelCalibration function requires a grouping variable and compares the accuracy of the observed default rate in the group with the average predicted PD for the group. For example, you can group by calendar year using the 'Year' variable.

CalMeasure = modelCalibration(pdModel,data(TestDataInd,:),'Year',DataID='test data'); disp(CalMeasure)

RMSE

________

Logistic, grouped by Year, test data 0.000453

Use modelCalibrationPlot to visualize the observed default rates compared to the predicted probabilities of default (PD).

modelCalibrationPlot(pdModel,data(TestDataInd,:),'Year',DataID='test data');

More About

References

[1] Baesens, Bart, Daniel Roesch, and Harald Scheule. Credit Risk Analytics: Measurement Techniques, Applications, and Examples in SAS. Wiley, 2016.

[2] Bellini, Tiziano. IFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SAS. San Diego, CA: Elsevier, 2019.

[3] Breeden, Joseph. Living with CECL: The Modeling Dictionary. Santa Fe, NM: Prescient Models LLC, 2018.

[4] Roesch, Daniel and Harald Scheule. Deep Credit Risk: Machine Learning with Python. Independently published, 2020.

Version History

Introduced in R2020bSee Also

Functions

Topics

- Basic Lifetime PD Model Validation

- Compare Logistic Model for Lifetime PD to Champion Model

- Compare Lifetime PD Models Using Cross-Validation

- Expected Credit Loss Computation

- Compare Model Discrimination and Model Calibration to Validate of Probability of Default

- Compare Probability of Default Using Through-the-Cycle and Point-in-Time Models

- Create Weighted Lifetime PD Model

- Overview of Lifetime Probability of Default Models