incrementalRegressionLinear

Linear regression model for incremental learning

Description

incrementalRegressionLinear creates an incrementalRegressionLinear model object, which represents an incremental linear model for regression problems. Supported learners include support vector machine (SVM) and least squares.

Unlike other Statistics and Machine Learning Toolbox™ model objects, incrementalRegressionLinear can be called directly. Also, you can specify learning options, such as performance metrics configurations, parameter values, and the objective solver, before fitting the model to data. After you create an incrementalRegressionLinear object, it is prepared for incremental learning.

incrementalRegressionLinear is best suited for incremental learning. For a traditional approach to training an SVM or linear regression model (such as creating a model by fitting it to data, performing cross-validation, tuning hyperparameters, and so on), see fitrsvm or fitrlinear.

Creation

You can create an incrementalRegressionLinear model object in several ways:

Call the function directly — Configure incremental learning options, or specify initial values for linear model parameters and hyperparameters, by calling

incrementalRegressionLineardirectly. This approach is best when you do not have data yet or you want to start incremental learning immediately.Convert a traditionally trained model — To initialize an linear regression model for incremental learning using the model coefficients and hyperparameters of a trained model object, you can convert the traditionally trained model to an

incrementalRegressionLinearmodel object by passing it to theincrementalLearnerfunction. This table contains links to the appropriate reference pages.Convertible Model Object Conversion Function RegressionSVMorCompactRegressionSVMincrementalLearnerRegressionLinearincrementalLearnerCall an incremental learning function —

fit,updateMetrics, andupdateMetricsAndFitaccept a configuredincrementalRegressionLinearmodel object and data as input, and return anincrementalRegressionLinearmodel object updated with information learned from the input model and data.

Description

Mdl = incrementalRegressionLinear()Mdl.

Properties of a default model contain placeholders for unknown model parameters. You must

train a default model before you can track its performance or generate predictions from

it.

Mdl = incrementalRegressionLinear(Name=Value)incrementalRegressionLinear(Beta=[0.1

0.3],Bias=1,MetricsWarmupPeriod=100) sets the vector of linear model

coefficients β to [0.1 0.3], the bias

β0 to 1, and the metrics

warm-up period to 100.

Name-Value Arguments

Properties

Object Functions

fit | Train linear model for incremental learning |

updateMetricsAndFit | Update performance metrics in linear incremental learning model given new data and train model |

updateMetrics | Update performance metrics in linear incremental learning model given new data |

loss | Loss of linear incremental learning model on batch of data |

predict | Predict responses for new observations from linear incremental learning model |

perObservationLoss | Per observation regression error of model for incremental learning |

reset | Reset incremental regression model |

Examples

Create a default incremental linear model for regression.

Mdl = incrementalRegressionLinear()

Mdl =

incrementalRegressionLinear

IsWarm: 0

Metrics: [1×2 table]

ResponseTransform: 'none'

Beta: [0×1 double]

Bias: 0

Learner: 'svm'

Properties, Methods

Mdl.EstimationPeriod

ans = 1000

Mdl is an incrementalRegressionLinear model object. All its properties are read-only.

Mdl must be fit to data before you can use it to perform any other operations. The software sets the estimation period to 1000 because half the width of the epsilon insensitive band Epsilon is unknown. You can set Epsilon to a positive floating-point scalar by using the Epsilon name-value argument. This action results in a default estimation period of 0.

Load the robot arm data set.

load robotarmFor details on the data set, enter Description at the command line.

Fit the incremental model to the training data by using the updateMetricsAndFit function. To simulate a data stream fit the model in chunks of 50 observations at a time. At each iteration:

Process 50 observations.

Overwrite the previous incremental model with a new one fitted to the incoming observations.

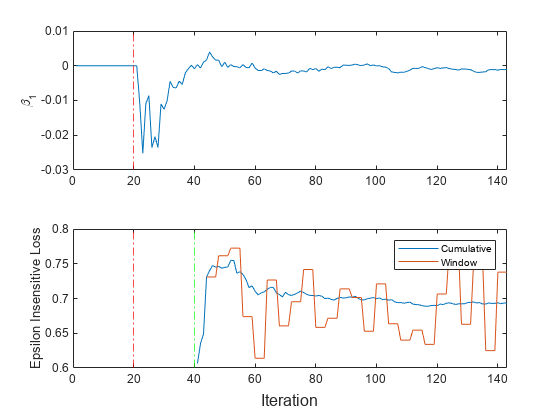

Store , the cumulative metrics, and the window metrics to see how they evolve during incremental learning.

% Preallocation n = numel(ytrain); numObsPerChunk = 50; nchunk = floor(n/numObsPerChunk); ei = array2table(zeros(nchunk,2),'VariableNames',["Cumulative" "Window"]); beta1 = zeros(nchunk+1,1); % Incremental fitting rng("default"); % For reproducibility for j = 1:nchunk ibegin = min(n,numObsPerChunk*(j-1) + 1); iend = min(n,numObsPerChunk*j); idx = ibegin:iend; Mdl = updateMetricsAndFit(Mdl,Xtrain(idx,:),ytrain(idx)); ei{j,:} = Mdl.Metrics{"EpsilonInsensitiveLoss",:}; beta1(j + 1) = Mdl.Beta(1); end

Mdl is an incrementalRegressionLinear model object trained on all the data in the stream. While updateMetricsAndFit processes the first 1000 observations, it stores the response values to estimate Epsilon; the function does not fit the coefficients until after this estimation period. During incremental learning and after the model is warmed up, updateMetricsAndFit checks the performance of the model on the incoming observations, and then fits the model to those observations.

To see how the performance metrics and evolve during training, plot them on separate tiles.

t = tiledlayout(2,1); nexttile plot(beta1) ylabel('\beta_1') xlim([0 nchunk]) xline(Mdl.EstimationPeriod/numObsPerChunk,'r-.') nexttile h = plot(ei.Variables); xlim([0 nchunk]) ylabel('Epsilon Insensitive Loss') xline(Mdl.EstimationPeriod/numObsPerChunk,'r-.') xline((Mdl.EstimationPeriod + Mdl.MetricsWarmupPeriod)/numObsPerChunk,'g-.') legend(h,ei.Properties.VariableNames) xlabel(t,'Iteration')

The plot suggests that updateMetricsAndFit does the following:

After the estimation period (first 20 iterations), fit during all incremental learning iterations.

Compute the performance metrics after the metrics warm-up period only.

Compute the cumulative metrics during each iteration.

Compute the window metrics after processing 500 observations (4 iterations).

Prepare an incremental regression learner by specifying a metrics warm-up period, during which the updateMetricsAndFit function only fits the model. Specify a metrics window size of 500 observations. Train the model by using SGD, and adjust the SGD batch size, learning rate, and regularization parameter.

Load the robot arm data set.

load robotarm

n = numel(ytrain);For details on the data set, enter Description at the command line.

Create an incremental linear model for regression. Configure the model as follows:

Specify the SGD solver.

Assume that these settings work well for the problem: a ridge regularization parameter value of 0.001, SGD batch size of 20, learning rate of 0.002, and half the width of the epsilon insensitive band for SVM of 0.05.

Specify that the incremental fitting functions process the raw (unstandardized) predictor data.

Specify a metrics warm-up period of 1000 observations.

Specify a metrics window size of 500 observations.

Track the epsilon insensitive loss, MSE, and mean absolute error (MAE) to measure the performance of the model. The software supports epsilon insensitive loss and MSE. Create an anonymous function that measures the absolute error of each new observation. Create a structure array containing the name

MeanAbsoluteErrorand its corresponding function.

maefcn = @(z,zfit)abs(z - zfit); maemetric = struct("MeanAbsoluteError",maefcn); Mdl = incrementalRegressionLinear('Epsilon',0.05, ... 'Solver','sgd','Lambda',0.001,'BatchSize',20,'LearnRate',0.002, ... 'Standardize',false, ... 'MetricsWarmupPeriod',1000,'MetricsWindowSize',500, ... 'Metrics',{'epsiloninsensitive' 'mse' maemetric})

Mdl =

incrementalRegressionLinear

IsWarm: 0

Metrics: [3×2 table]

ResponseTransform: 'none'

Beta: [0×1 double]

Bias: 0

Learner: 'svm'

Properties, Methods

Mdl is an incrementalRegressionLinear model object configured for incremental learning without an estimation period.

Fit the incremental model to the data by using the updateMetricsAndFit function. At each iteration:

Simulate a data stream by processing a chunk of 50 observations. Note that the chunk size is different from SGD batch size.

Overwrite the previous incremental model with a new one fitted to the incoming observations.

Store the estimated coefficient , the cumulative metrics, and the window metrics to see how they evolve during incremental learning.

% Preallocation numObsPerChunk = 50; nchunk = floor(n/numObsPerChunk); ei = array2table(zeros(nchunk,2),'VariableNames',["Cumulative" "Window"]); mse = array2table(zeros(nchunk,2),'VariableNames',["Cumulative" "Window"]); mae = array2table(zeros(nchunk,2),'VariableNames',["Cumulative" "Window"]); beta10 = zeros(nchunk+1,1); % Incremental fitting rng("default"); % For reproducibility for j = 1:nchunk ibegin = min(n,numObsPerChunk*(j-1) + 1); iend = min(n,numObsPerChunk*j); idx = ibegin:iend; Mdl = updateMetricsAndFit(Mdl,Xtrain(idx,:),ytrain(idx)); ei{j,:} = Mdl.Metrics{"EpsilonInsensitiveLoss",:}; mse{j,:} = Mdl.Metrics{"MeanSquaredError",:}; mae{j,:} = Mdl.Metrics{"MeanAbsoluteError",:}; beta10(j + 1) = Mdl.Beta(10); end

Mdl is an incrementalRegressionLinear model object trained on all the data in the stream. During incremental learning and after the model is warmed up, updateMetricsAndFit checks the performance of the model on the incoming observations, and then fits the model to those observations.

To see how the performance metrics and evolve during training, plot them on separate tiles.

tiledlayout(2,2) nexttile plot(beta10) ylabel('\beta_{10}') xlim([0 nchunk]) xline(Mdl.MetricsWarmupPeriod/numObsPerChunk,'g-.') xlabel('Iteration') nexttile h = plot(ei.Variables); xlim([0 nchunk]) ylabel('Epsilon Insensitive Loss') xline(Mdl.MetricsWarmupPeriod/numObsPerChunk,'g-.') legend(h,ei.Properties.VariableNames) xlabel('Iteration') nexttile h = plot(mse.Variables); xlim([0 nchunk]) ylabel('MSE') xline(Mdl.MetricsWarmupPeriod/numObsPerChunk,'g-.') legend(h,mse.Properties.VariableNames) xlabel('Iteration') nexttile h = plot(mae.Variables); xlim([0 nchunk]) ylabel('MAE') xline(Mdl.MetricsWarmupPeriod/numObsPerChunk,'g-.') legend(h,mae.Properties.VariableNames) xlabel('Iteration')

The plot suggests that updateMetricsAndFit does the following:

Fit during all incremental learning iterations.

Compute the performance metrics after the metrics warm-up period only.

Compute the cumulative metrics during each iteration.

Compute the window metrics after processing 500 observations (10 iterations).

Train a linear regression model by using fitrlinear, convert it to an incremental learner, track its performance, and fit it to streaming data. Carry over training options from traditional to incremental learning.

Load and Preprocess Data

Load the 2015 NYC housing data set, and shuffle the data. For more details on the data, see NYC Open Data.

load NYCHousing2015 rng(1); % For reproducibility n = size(NYCHousing2015,1); idxshuff = randsample(n,n); NYCHousing2015 = NYCHousing2015(idxshuff,:);

Suppose that the data collected from Manhattan (BOROUGH = 1) was collected using a new method that doubles its quality. Create a weight variable that attributes 2 to observations collected from Manhattan, and 1 to all other observations.

NYCHousing2015.W = ones(n,1) + (NYCHousing2015.BOROUGH == 1);

Extract the response variable SALEPRICE from the table. For numerical stability, scale SALEPRICE by 1e6.

Y = NYCHousing2015.SALEPRICE/1e6; NYCHousing2015.SALEPRICE = [];

Create dummy variable matrices from the categorical predictors.

catvars = ["BOROUGH" "BUILDINGCLASSCATEGORY" "NEIGHBORHOOD"]; dumvarstbl = varfun(@(x)dummyvar(categorical(x)),NYCHousing2015, ... 'InputVariables',catvars); dumvarmat = table2array(dumvarstbl); NYCHousing2015(:,catvars) = [];

Treat all other numeric variables in the table as linear predictors of sales price. Concatenate the matrix of dummy variables to the rest of the predictor data. Transpose the resulting predictor matrix.

idxnum = varfun(@isnumeric,NYCHousing2015,'OutputFormat','uniform'); X = [dumvarmat NYCHousing2015{:,idxnum}]';

Train Linear Regression Model

Fit a linear regression model to a random sample of half the data.

idxtt = randsample([true false],n,true); TTMdl = fitrlinear(X(:,idxtt),Y(idxtt),'ObservationsIn','columns', ... 'Weights',NYCHousing2015.W(idxtt))

TTMdl =

RegressionLinear

ResponseName: 'Y'

ResponseTransform: 'none'

Beta: [313×1 double]

Bias: 0.1116

Lambda: 2.1977e-05

Learner: 'svm'

Properties, Methods

TTMdl is a RegressionLinear model object representing a traditionally trained linear regression model.

Convert Trained Model

Convert the traditionally trained linear regression model to a linear regression model for incremental learning.

IncrementalMdl = incrementalLearner(TTMdl)

IncrementalMdl =

incrementalRegressionLinear

IsWarm: 1

Metrics: [1×2 table]

ResponseTransform: 'none'

Beta: [313×1 double]

Bias: 0.1116

Learner: 'svm'

Properties, Methods

Separately Track Performance Metrics and Fit Model

Perform incremental learning on the rest of the data by using the updateMetrics and fit functions. Simulate a data stream by processing 500 observations at a time. At each iteration:

Call

updateMetricsto update the cumulative and window epsilon insensitive loss of the model given the incoming chunk of observations. Overwrite the previous incremental model to update the losses in theMetricsproperty. Note that the function does not fit the model to the chunk of data—the chunk is "new" data for the model. Specify that the observations are oriented in columns, and specify the observation weights.Call

fitto fit the model to the incoming chunk of observations. Overwrite the previous incremental model to update the model parameters. Specify that the observations are oriented in columns, and specify the observation weights.Store the losses and last estimated coefficient .

% Preallocation idxil = ~idxtt; nil = sum(idxil); numObsPerChunk = 500; nchunk = floor(nil/numObsPerChunk); ei = array2table(zeros(nchunk,2),'VariableNames',["Cumulative" "Window"]); beta313 = [IncrementalMdl.Beta(end); zeros(nchunk,1)]; Xil = X(:,idxil); Yil = Y(idxil); Wil = NYCHousing2015.W(idxil); % Incremental fitting for j = 1:nchunk ibegin = min(nil,numObsPerChunk*(j-1) + 1); iend = min(nil,numObsPerChunk*j); idx = ibegin:iend; IncrementalMdl = updateMetrics(IncrementalMdl,Xil(:,idx),Yil(idx), ... 'ObservationsIn','columns','Weights',Wil(idx)); ei{j,:} = IncrementalMdl.Metrics{"EpsilonInsensitiveLoss",:}; IncrementalMdl = fit(IncrementalMdl,Xil(:,idx),Yil(idx),'ObservationsIn','columns', ... 'Weights',Wil(idx)); beta313(j + 1) = IncrementalMdl.Beta(end); end

IncrementalMdl is an incrementalRegressionLinear model object trained on all the data in the stream.

Alternatively, you can use updateMetricsAndFit to update performance metrics of the model given a new chunk of data, and then fit the model to the data.

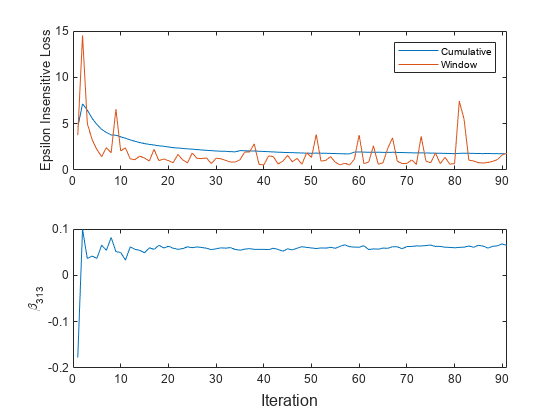

Plot a trace plot of the performance metrics and estimated coefficient .

t = tiledlayout(2,1); nexttile h = plot(ei.Variables); xlim([0 nchunk]) ylabel('Epsilon Insensitive Loss') legend(h,ei.Properties.VariableNames) nexttile plot(beta313) ylabel('\beta_{313}') xlim([0 nchunk]) xlabel(t,'Iteration')

The cumulative loss gradually changes with each iteration (chunk of 500 observations), whereas the window loss jumps. Because the metrics window is 200 by default, updateMetrics measures the performance based on the latest 200 observations in each 500 observation chunk.

changes abruptly, then levels off as fit processes chunks of observations.

More About

Tips

After creating a model, you can generate C/C++ code that performs incremental learning on a data stream. Generating C/C++ code requires MATLAB Coder™. For details, see Introduction to Code Generation.

Algorithms

References

Extended Capabilities

Version History

Introduced in R2020b

See Also

Functions

fit|updateMetrics|updateMetricsAndFit|predict|incrementalLearner (RegressionLinear)|incrementalLearner (RegressionSVM)