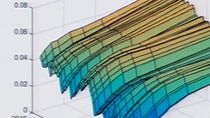

How to Price Interest Rate Options with Negative Interest Rates

Using a normal volatility model, a shifted Black model, or a shifted SABR model, you can price interest rate options with negative interest rates in MATLAB® and Financial Instruments Toolbox™.

You can also select a web site from the following list

How to Get Best Site Performance

Select the China site (in Chinese or English) for best site performance. Other MathWorks country sites are not optimized for visits from your location.