Perform ARIMA Model Residual Diagnostics Using Econometric Modeler App

This example shows how to evaluate ARIMA model assumptions by

performing residual diagnostics in the Econometric Modeler app. The data set, which

is stored in Data_JAustralian.mat, contains the log quarterly

Australian Consumer Price Index (CPI) measured from 1972 and 1991, among other time

series.

Import Data into Econometric Modeler

At the command line, load the Data_JAustralian.mat data

set.

load Data_JAustralianAt the command line, open the Econometric Modeler app.

econometricModeler

Alternatively, open the app from the apps gallery (see Econometric Modeler).

Import DataTimeTable into the app:

On the Modeler tab, in the Import section, click the Import button

.

.In the Import Data dialog box, select the check box for the

DataTimeTablevariable.Click Import.

The variables, including PAU, appear in the

Time Series pane, and a time series plot containing all

the series appears in the Plot(EXCH) figure window.

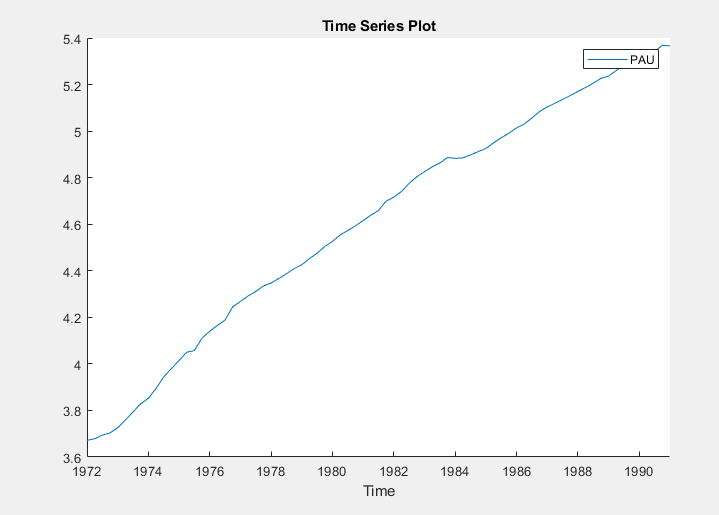

Create a time series plot of PAU by double-clicking

PAU in the Time Series

pane.

Specify and Estimate ARIMA Model

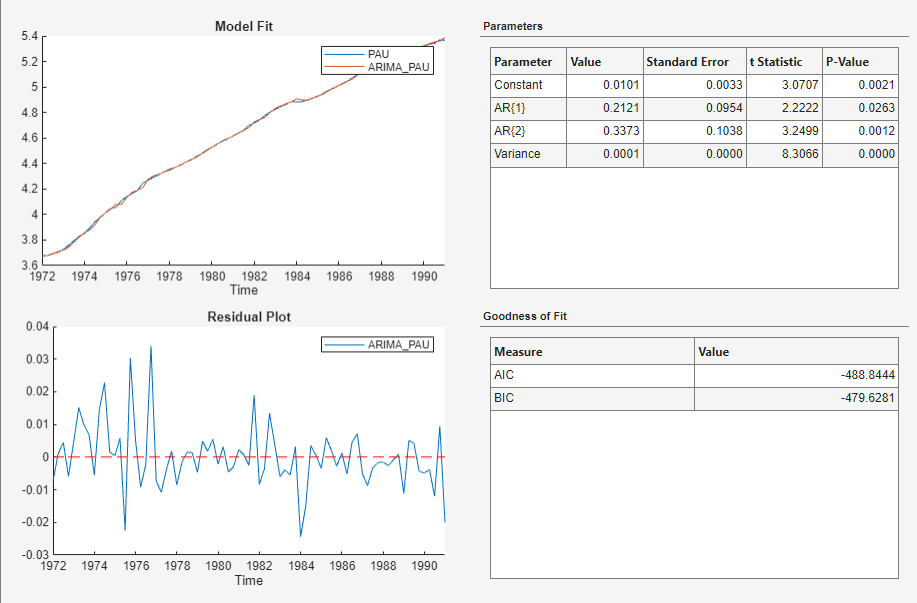

Estimate an ARIMA(2,1,0) model for the log quarterly Australian CPI (for details, see Implement Box-Jenkins Model Selection and Estimation Using Econometric Modeler App).

In the Time Series pane, select the

PAUtime series.On the Modeler tab, in the Models section, click ARIMA.

In the ARIMA Model Parameters dialog box, on the Lag Order tab:

Set the Autoregressive Order (p) to

2.Set the Moving Average Order (q) to

0.Click Estimate.

The model variable ARIMA_PAU appears in the

Models pane, its value appears in the

Preview pane, and its estimation summary appears in the

Fit(ARIMA_PAU) document.

In the Fit(ARIMA_PAU) document, the Residual Plot figure is a time series plot of the residuals. The plot suggests that the residuals are centered at y = 0 and they exhibit volatility clustering.

Perform Residual Diagnostics

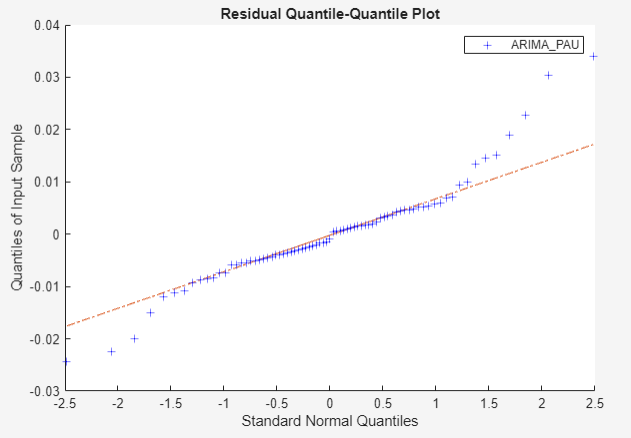

Visually assess whether the residuals are normally distributed by plotting their histogram and a quantile-quantile plot:

Close the Fit(ARIMA_PAU) document.

With

ARIMA_PAUselected in the Models pane, on the Modeler tab, in the Diagnostics section, click Model Fit Diagnostics > Residual Histogram.Click Model Fit Diagnostics > Residual Q-Q Plot.

Inspect the histogram by clicking the Hist(ARIMA_PAU) figure window.

Inspect the quantile-quantile plot by clicking the QQ(ARIMA_PAU) figure window.

The residuals appear approximately normally distributed. However, there is an excess of large residuals, which indicates that a t innovation distribution might be a reasonable model modification.

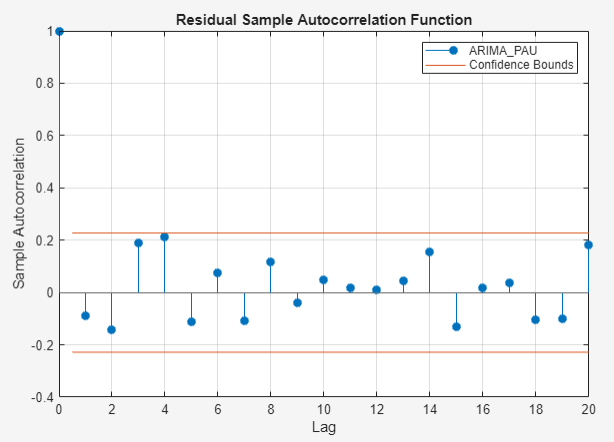

Visually assess whether the residuals are serially correlated by plotting

their autocorrelations. With ARIMA_PAU selected in

the Models pane, in the Diagnostics

section, click Model Fit Diagnostics >

Residual Autocorrelation.

All lags that are greater than 0 correspond to insignificant autocorrelations. Therefore, the residuals are uncorrelated in time.

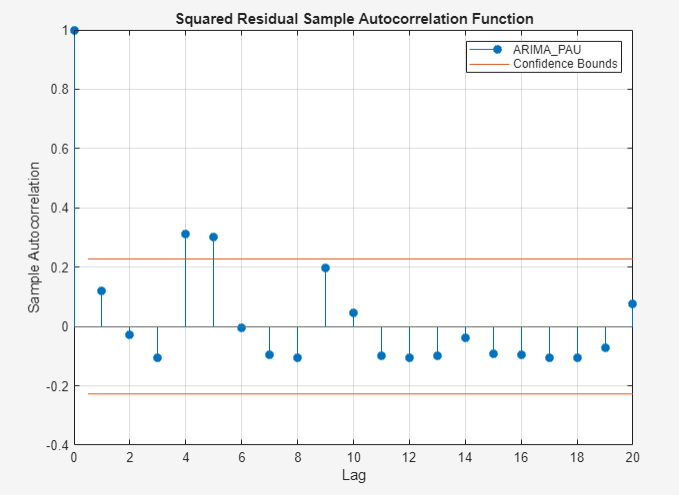

Visually assess whether the residuals exhibit heteroscedasticity by plotting

the ACF of the squared residuals. With ARIMA_PAU

selected in the Models pane, click the

Modeler tab. Then, click the

Diagnostics section, click Model Fit

Diagnostics > Squared Residual

Autocorrelation.

Significant autocorrelations occur at lags 4 and 5, which suggests a composite

conditional mean and variance model for PAU.

See Also

Apps

Objects

Functions

Topics

- Infer Residuals for Diagnostic Checking

- Perform GARCH Model Residual Diagnostics Using Econometric Modeler App

- Implement Box-Jenkins Model Selection and Estimation Using Econometric Modeler App

- Specify t Innovation Distribution Using Econometric Modeler App

- Creating ARIMA Models Using Econometric Modeler App