Detect ARCH Effects Using Econometric Modeler App

These examples show how to assess whether a series has volatility clustering by using

the Econometric Modeler app. Methods include inspecting correlograms of

squared residuals and testing for significant ARCH lags. The data set, stored in

Data_EquityIdx.mat, contains a series of daily NASDAQ closing

prices from 1990 through 2001.

Inspect Correlograms of Squared Residuals for ARCH Effects

This example shows how to visually determine whether a series has significant ARCH effects by plotting the autocorrelation function (ACF) and partial autocorrelation function (PACF) of a series of squared residuals.

At the command line, load the Data_EquityIdx.mat data

set.

load Data_EquityIdxThe data set contains a table of NASDAQ and NYSE closing prices, among

other variables. For more details about the data set, enter

Description at the command line.

At the command line, open the Econometric Modeler app.

econometricModeler

Alternatively, open the app from the apps gallery (see Econometric Modeler).

Import DataTimeTable into the app:

On the Modeler tab, in the Import section, click the Import button

.

.In the Import Data dialog box, select the check box for the

DataTimeTablevariable.Click Import.

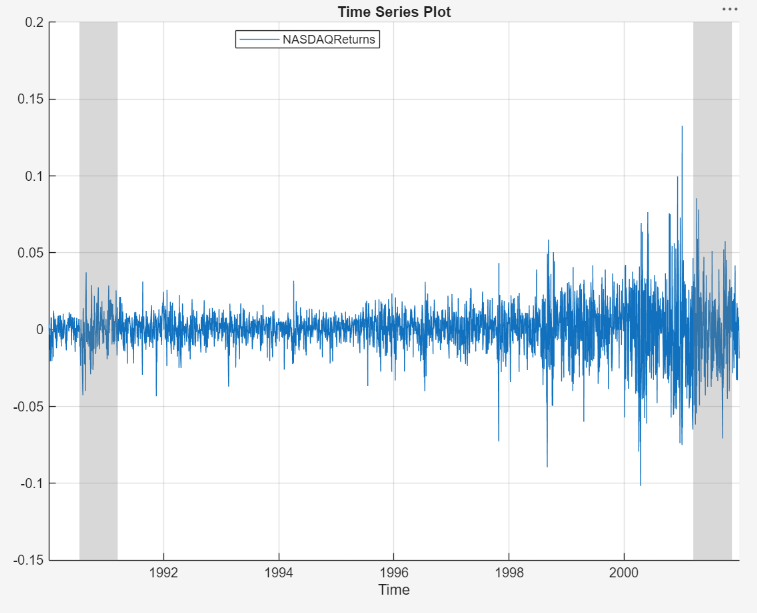

The variables appear in the Time Series pane, and a time series plot of all the series appears in the Plot(NASDAQ) figure window.

Convert the daily close NASDAQ index series to a percentage return series by taking the log of the series, then taking the first difference of the logged series:

In the Time Series pane, select

NASDAQ.On the Modeler tab, in the Transforms section, click Log.

With

NASDAQ_Logselected, in the Transforms section, click Difference.In the Time Series pane, rename the

NASDAQ_Log_Diffvariable by clicking it twice to select its name and enteringNASDAQReturns.

The time series plot of the NASDAQ returns appears in the Plot(NASDAQReturns) figure window.

The returns appear to fluctuate around a constant level, but exhibit volatility clustering. Large changes in the returns tend to cluster together, and small changes tend to cluster together. That is, the series exhibits conditional heteroscedasticity.

Compute squared residuals:

Export

NASDAQReturnsto the MATLAB® Workspace:In the Time Series pane, right-click

NASDAQReturns.In the context menu, select Export.

NASDAQReturnsappears in the MATLAB Workspace.At the command line:

For numerical stability, scale the returns by a factor of 100.

Create a residual series by removing the mean from the scaled returns series. Because you took the first difference of the NASDAQ prices to create the returns, the first element of the returns is missing. Therefore, to estimate the sample mean of the series, call

mean(NASDAQReturns,'omitnan').Square the residuals.

Add the squared residuals as a new variable to the

DataTimeTabletimetable.

NASDAQReturns = 100*NASDAQReturns; NASDAQResiduals = NASDAQReturns - mean(NASDAQReturns,"omitnan"); NASDAQResiduals2 = NASDAQResiduals.^2; DataTimeTable.NASDAQResiduals2 = NASDAQResiduals2;

In Econometric Modeler, import DataTimeTable:

On the Modeler tab, in the Import section, click

.In the Econometric Modeler dialog box, click OK to clear all variables and documents in the app.

In the Import Data dialog box, select the check box for

DataTimeTable.Click Import.

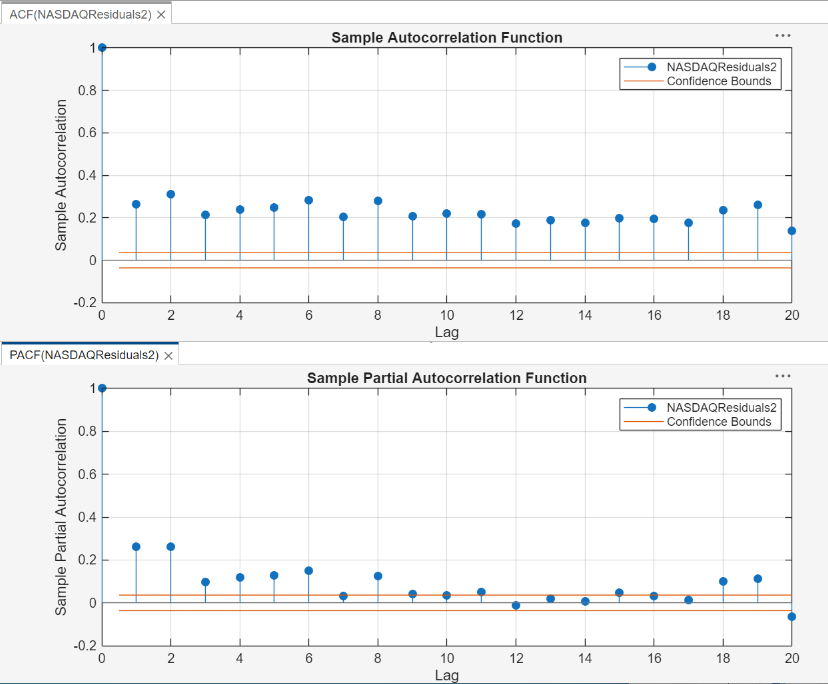

Plot the ACF and PACF:

In the Time Series pane, select the

NASDAQResiduals2time series.Click the Plots tab, then click ACF.

Click the Plots tab, then click PACF.

Close the Plot(NASDAQ) figure window. Then, position the ACF(NASDAQResiduals2) figure window above the PACF(NASDAQResiduals2) figure window.

The sample ACF and PACF show significant autocorrelation in the squared residuals. This result indicates that volatility clustering is present.

Conduct Ljung-Box Q-Test on Squared Residuals

This example shows how to test squared residuals for significant ARCH effects using the Ljung-Box Q-test.

At the command line:

Load the

Data_EquityIdx.matdata set.Convert the NASDAQ prices to returns. To maintain the correct time base, prepend the resulting returns with a

NaNvalue.Scale the NASDAQ returns.

Compute residuals by removing the mean from the scaled returns.

Square the residuals.

Add the vector of squared residuals as a variable to

DataTimeTable.

For more details on the steps, see Inspect Correlograms of Squared Residuals for ARCH Effects.

load Data_EquityIdx NASDAQReturns = 100*price2ret(DataTimeTable.NASDAQ); NASDAQReturns = [NaN; NASDAQReturns]; NASDAQResiduals2 = (NASDAQReturns - mean(NASDAQReturns,"omitnan")).^2; DataTimeTable.NASDAQResiduals2 = NASDAQResiduals2;

At the command line, open the Econometric Modeler app.

econometricModeler

Alternatively, open the app from the apps gallery (see Econometric Modeler).

Import DataTimeTable into the app:

On the Modeler tab, in the Import section, click the Import button

.In the Import Data dialog box, select the check box for the

DataTimeTablevariable.Click Import.

The variables appear in the Time Series pane, and a time series plot of all the series appears in the Plot(NASDAQ) figure window.

Test the null hypothesis that the first m = 5 autocorrelation lags of the squared residuals are jointly zero by using the Ljung-Box Q-test. Then, test the null hypothesis that the first m = 10 autocorrelation lags of the squared residuals are jointly zero.

In the Time Series pane, select the

NASDAQResiduals2time series.On the Modeler tab, in the Tests section, click Add Test > Ljung-Box Q-Test.

On the LBQ tab, in the Settings section, set both the Number of Lags and DOF to

5. To maintain a significance level of 0.05 for the two tests, set Significance Level to 0.025.In the Tests section, click Run Test.

Repeat steps 3 and 4, but set both the Number of Lags and DOF to

10instead.

The test results appear in the Results table of the LBQ(NASDAQResiduals2) document.

The null hypothesis is rejected for the two tests. The p-value for each test is 0. The results show that not every autocorrelation up to lag 5 (or 10) is zero, indicating volatility clustering in the squared residuals.

Conduct Engle's ARCH Test

This example shows how to test residuals for significant ARCH effects using the Engle's ARCH Test.

At the command line:

Load the

Data_EquityIdx.matdata set.Convert the NASDAQ prices to returns. To maintain the correct time base, prepend the resulting returns with a

NaNvalue.Scale the NASDAQ returns.

Compute residuals by removing the mean from the scaled returns.

Add the vector of residuals as a variable to

DataTimeTable.

For more details on the steps, see Inspect Correlograms of Squared Residuals for ARCH Effects.

load Data_EquityIdx NASDAQReturns = 100*price2ret(DataTimeTable.NASDAQ); NASDAQReturns = [NaN; NASDAQReturns]; NASDAQResiduals = NASDAQReturns - mean(NASDAQReturns,"omitnan"); DataTimeTable.NASDAQResiduals = NASDAQResiduals;

At the command line, open the Econometric Modeler app.

econometricModeler

Alternatively, open the app from the apps gallery (see Econometric Modeler).

Import DataTimeTable into the app:

On the Modeler tab, in the Import section, click the Import button

.In the Import Data dialog box, select the check box for the

DataTimeTablevariable.Click Import.

The variables appear in the Time Series pane, and a time series plot of the all the series appears in the Plot(NASDAQ) figure window.

Test the null hypothesis that the NASDAQ residuals series exhibits no ARCH effects by using Engle's ARCH test. Specify that the residuals series is an ARCH(2) model.

In the Time Series pane, select the

NASDAQResidualstime series.On the Modeler tab, in the Tests section, click Add Test > Engle's ARCH Test.

On the ARCH tab, in the Settings section, set Number of Lags to

2.In the Tests section, click Run Test.

The test results appear in the Results table of the ARCH(NASDAQResiduals) document.

The null hypothesis is rejected in favor of the ARCH(2) alternative. The test result indicates significant volatility clustering in the residuals.