portfolioCostCurves

Estimate market-impact cost of order execution for portfolio

Description

pcc = portfolioCostCurves(k,portfolio,tradeQuantity,tqRange,tradeStrategy,tsRange)

Kissell Research Group (KRG) transaction cost analysis object

kPortfolio data

portfolioTrade quantity

tradeQuantitywith a range of valuestqRangeTrade strategy

tradeStrategywith a range of valuestsRange

Examples

Retrieve the market impact data from the KRG FTP site. Connect to the FTP site using the

ftp function with a user name and password. Navigate to the

MI_Parameters folder and retrieve the market impact data in the

MI_Encrypted_Parameters.csv file. miData contains

the encrypted market impact date, code, and parameters.

f = ftp('ftp.kissellresearch.com','username','pwd'); mget(f,'MI_Encrypted_Parameters.csv'); miData = readtable('MI_Encrypted_Parameters.csv','delimiter', ... ',','ReadRowNames',false,'ReadVariableNames',true);

Create a Kissell Research Group transaction cost analysis object

k.

k = krg(miData);

Load the example portfolio data from the file

KRGExampleData.mat, which is included with the

Datafeed Toolbox™.

load KRGExampleDataThe variable PortfolioData appears in the MATLAB® workspace.

PortfolioData contains these variables:

Stock symbol

Local price

Price in a different currency if applicable

Average daily volume

Volatility

Number of shares

For a description of the example data, see Interpret Variables in Kissell Research Group Data Sets.

Estimate market-impact cost for an order execution on

a portfolio of assets. Specify the trade quantity as DollarValue.

Specify the trade quantity range tqRange with increments

of $10,000,000. Start with a total portfolio value of $100,000,000

and end with $500,000,000. Set the percentage of volume trading strategy POV.

Specify the trade strategy range tsRange with increments

of 10% by starting with a percentage of volume of 10% and ending with

40%.

tqRange = (100000000:10000000:500000000); tsRange = (0.10:0.10:0.40); pcc = portfolioCostCurves(k,PortfolioData,'DollarValue',tqRange,... 'POV',tsRange);

Display the first three rows of market-impact cost data.

pcc(1:3,:)

ans =

Size Shares TradeValue AbsTradeValue POV TradeTime Cost_bp Cost_DollarsPerShare Cost_Dollars

____ __________ ____________ _____________ ____ _________ _______ ____________________ ____________

0.02 5612057.03 100000000.00 328737579.09 0.10 0.18 38.74 0.07 387447.95

0.02 5612057.03 100000000.00 328737579.09 0.20 0.08 61.18 0.11 611819.30

0.02 5612057.03 100000000.00 328737579.09 0.30 0.05 80.07 0.14 800683.38

The market-impact cost data contains:

Average trade size across all stocks in the portfolio

Number of shares in the transaction

Sum of traded value across all stocks in the portfolio

Sum of absolute value of the trade value across all stocks in the portfolio

Average execution percentage of volume to complete the number of shares

Average trade time in percentage of the day to complete the number of shares

Market-impact cost in basis points of local price

Market-impact cost in dollars per share

Market-impact cost in total dollar value

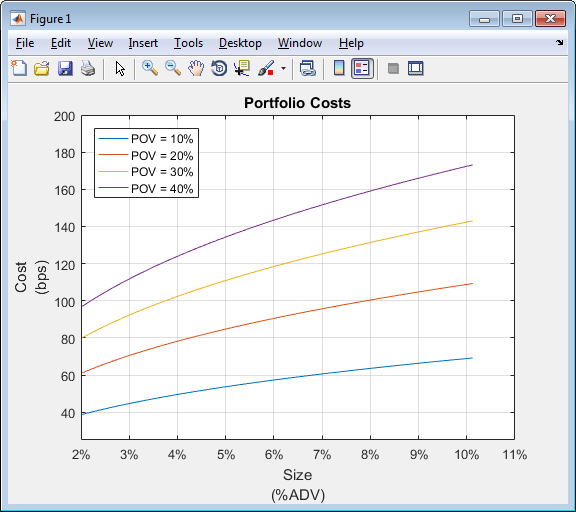

Display portfolio cost curves for percentage of volume rates: 10%, 20%, 30%, and 40%.

figure size10 = pcc.Size(1:4:end)*100; size20 = pcc.Size(2:4:end)*100; size30 = pcc.Size(3:4:end)*100; size40 = pcc.Size(4:4:end)*100; cost10 = pcc.Cost_bp(1:4:end); cost20 = pcc.Cost_bp(2:4:end); cost30 = pcc.Cost_bp(3:4:end); cost40 = pcc.Cost_bp(4:4:end); plot(size10,cost10,size20,cost20,size30,cost30,size40,cost40) grid on axis([2 11 25 200]) xlabel({'Size','(%ADV)'}) ylabel({'Cost','(bps)'}) legend('POV = 10%','POV = 20%','POV = 30%','POV = 40%',... 'Location','northwest') title('Portfolio Costs') a = gca; a.XAxis.TickLabelFormat = '%g%%';

This figure demonstrates using portfolio costs to construct the portfolio and manage portfolio contents. By analyzing portfolio costs, you can determine the optimal portfolio size.

Input Arguments

Output Arguments

Tips

To test multiple portfolio transactions, you can use different ranges. You can change the percentage of shares in the transaction or use a different trade strategy. For details, see Input Arguments.

For details about the calculations, contact Kissell Research Group.

References

[1] Kissell, Robert. “A Practical Framework for Transaction Cost Analysis.” Journal of Trading. Vol. 3, Number 2, Summer 2008, pp. 29–37.

[2] Kissell, Robert. “Algorithmic Trading Strategies.” Ph.D. Thesis. Fordham University, May 2006.

[3] Kissell, Robert. “TCA in the Investment Process: An Overview.” Journal of Index Investing. Vol. 2, Number 1, Summer 2011, pp. 60–64.

[4] Kissell, Robert. The Science of Algorithmic Trading and Portfolio Management. Cambridge, MA: Elsevier/Academic Press, 2013.

[5] Kissell, Robert, and Morton Glantz. Optimal Trading Strategies. New York, NY: AMACOM, Inc., 2003.

Version History

Introduced in R2016a

See Also

krg | costCurves | iStar | marketImpact | timingRisk